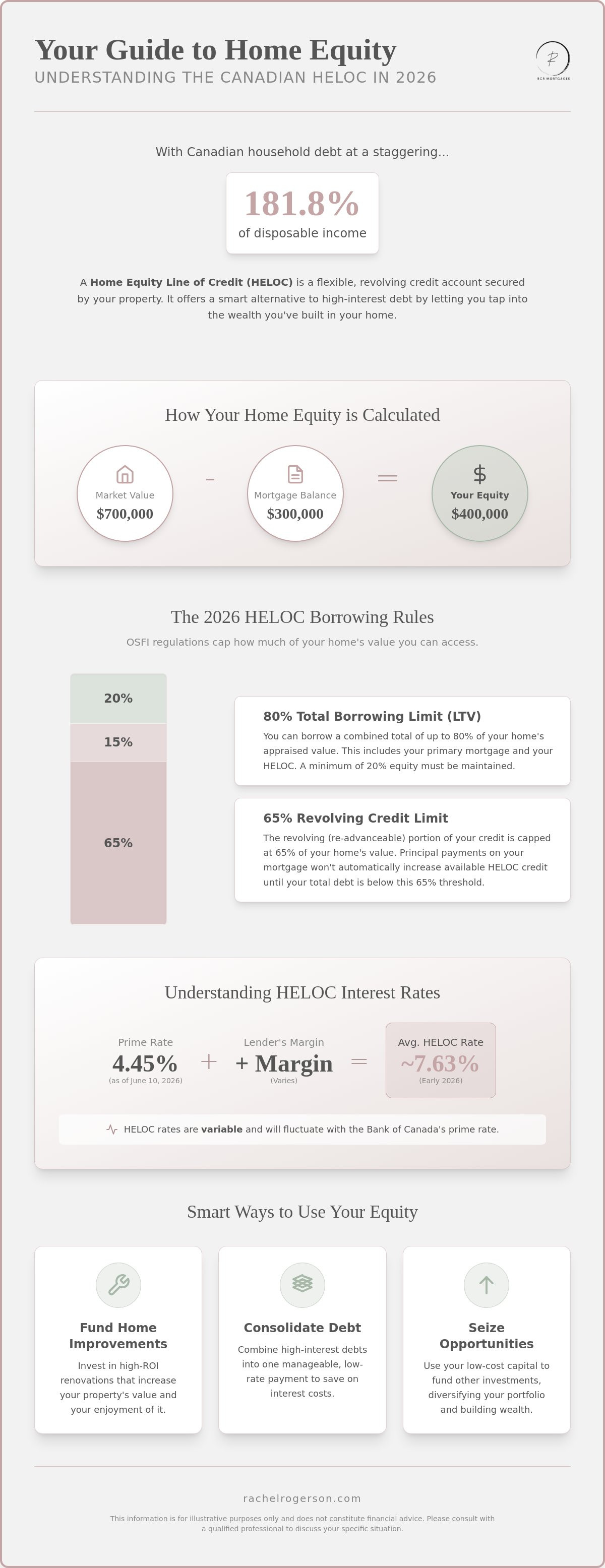

With Canadian household debt sitting at a staggering 181.8 percent of disposable income, is your home's equity your greatest asset or a missed opportunity for financial relief? You've likely realized that as interest rates stay higher for longer, a home equity line of credit offers a much-needed alternative to expensive credit card debt. It's stressful to see your property value climb while your monthly budget feels increasingly squeezed. You need a smarter way to access capital that doesn't involve high-interest traps.

We understand that the shifting rules around borrowing can feel overwhelming, especially with the latest OSFI regulations capping re-advanceable portions at 65 percent. This guide will help you master the mechanics of your home's value so you can fund renovations, consolidate debt, or invest with confidence. We'll clarify exactly how much you can borrow under the 2026 guidelines and provide a clear, efficient strategy to pay it back, ensuring your home remains your most secure investment.

Key Takeaways

- Learn how to leverage a revolving credit structure to borrow, repay, and reuse funds as your financial needs evolve without the hassle of re-applying.

- Understand the impact of the 2026 LTV limits and the 65 percent cap on re-advanceable credit to accurately calculate your true borrowing power.

- Determine if a home equity line of credit is the most cost-effective choice for your goals compared to a mortgage refinance or a reverse mortgage.

- Prepare for the mandatory stress test and organize your documentation to streamline the approval process and secure the best possible rates.

- Identify strategic ways to deploy your equity, from funding high-ROI home improvements to consolidating high-interest debt into a manageable, low-rate solution.

Understanding the Basics of a Home Equity Line of Credit

A home equity line of credit is a flexible financial tool that lets you tap into the wealth you've built in your property. Unlike a traditional mortgage that provides a single lump sum, a HELOC functions as a revolving credit account. You borrow what you need, pay it back, and can access those funds again without needing a new application. This flexibility is a primary reason why Canadian homeowners prefer it over fixed-term loans for ongoing projects. It's a dynamic resource that grows as you pay down your mortgage principal.

Why choose this over a standard credit card or a personal loan? The answer lies in the interest rate. Because a home equity line of credit is secured by your property, lenders view it as a lower-risk investment. This security translates to significantly lower interest rates than you'd find with unsecured debt. It's an efficient way to manage large expenses, like a major renovation or debt consolidation, while keeping your overall borrowing costs manageable. You only pay interest on the amount you actually use, not the entire limit available to you.

How Home Equity is Calculated in Canada

Equity is the portion of your home that you truly own. The formula is straightforward: Current Market Value minus your Outstanding Mortgage Balance. Let's look at a practical example. If your home has a market value of $700,000 and you still owe $300,000 on your mortgage, you have $400,000 in equity. Lenders use professional appraisals to verify the value of your property. These experts look at local market trends, the condition of your home, and recent sales in your neighbourhood to ensure the calculation is accurate. This figure forms the basis for how much you can eventually borrow.

The Role of Collateral and Security

Think of security as the foundation of your loan. A HELOC is "secured" because your home acts as collateral for the lender. This arrangement is what allows banks to offer those attractive, low interest rates. However, it's vital to understand the responsibility involved. If you can't manage the revolving credit and default on your payments, the lender has a legal claim to your property. This risk is why unsecured lines of credit have higher rates and lower limits; they don't have a physical asset backing them up. When you use your home as security, you're trading that asset's value for better terms and a higher level of financial freedom.

The Mechanics: How a HELOC Works in 2026

Understanding how a home equity line of credit functions requires a look at current federal regulations. In Canada, the Office of the Superintendent of Financial Institutions (OSFI) sets strict boundaries to protect both lenders and homeowners. While you can technically borrow up to 80 percent of your home's appraised value, there's a specific nuance to the "revolving" portion. Only 65 percent of your home’s value can be accessed as a revolving line of credit. If your total debt, which includes your mortgage and your line of credit, exceeds this 65 percent threshold, your principal mortgage payments won't automatically increase your available credit until the total balance drops below that cap.

These HELOC rules in Canada ensure that you maintain a healthy equity cushion. Most borrowers find the interest-only payment option particularly attractive for managing monthly cash flow. Since you aren't forced to pay down the principal immediately, you can keep your mandatory costs low during expensive periods, such as a major renovation. However, remember that your interest rate is variable. It fluctuates based on the Bank of Canada's prime rate, which currently sits at 4.45 percent as of June 10, 2026.

Standalone HELOC vs. Combined Mortgage-HELOC

Choosing the right structure depends on your existing mortgage status. A standalone HELOC is a separate product, often ideal for those who have already paid off their mortgage or hold it with a different lender. In contrast, a combined plan links your mortgage and credit line together. As you pay down your mortgage principal, your credit limit automatically increases, giving you instant access to your equity. This "re-advanceable" feature is a powerful wealth-building tool, though it's now subject to the stricter 65 percent LTV limit on the revolving portion to ensure long-term stability.

Interest Rates and Repayment Flexibility

Interest rates for a home equity line of credit are typically expressed as "Prime plus a margin," such as Prime + 0.5 percent. With average rates hovering around 7.63 percent in early 2026, it remains one of the most affordable ways to access large sums of capital. You enjoy total control over your repayment schedule. Unlike a traditional mortgage, you can pay off the entire balance at any time without facing prepayment penalties. If you're unsure which structure fits your financial goals, consulting with a specialist at Rachel Rogerson can provide the clarity you need. This level of flexibility allows you to treat your home equity like a strategic reserve, ready for whenever life presents a new opportunity or challenge.

HELOC vs. Refinance vs. Reverse Mortgage: Which is Right?

Choosing the right way to access your home's value depends on your specific goals and life stage. While a home equity line of credit offers unmatched flexibility, it isn't always the most cost-effective path for every situation. You might wonder if simply increasing your mortgage through a refinance is a better move. Let's look at the numbers. Setting up a HELOC often involves an appraisal fee between $300 and $600, plus legal and registration fees ranging from $500 to $1,500. While these costs are similar to those of a refinance, the long-term impact on your interest costs varies wildly depending on how you use the funds.

For many Canadians, the decision comes down to how they plan to spend the money. A line of credit is a tool for ongoing needs, whereas a refinance is a structural change to your primary debt. Rachel Rogerson Mortgage Broker specializes in helping homeowners, particularly seniors, navigate these specific choices to ensure the selected product aligns with their long-term wealth strategy. We don't just look at the interest rate; we look at the total cost of borrowing over the life of the loan.

When to Choose a Mortgage Refinance

If you need a large, one-time lump sum for a specific project, a mortgage refinance might be the superior choice. It allows you to lock in a fixed interest rate, providing stability that a variable-rate HELOC cannot offer. This is especially relevant when looking at HELOC rates and trends for 2026, which show that variable borrowing costs remain sensitive to market shifts. Be careful, though. Refinancing an existing mortgage before your term is up can trigger a "break fee" or prepayment penalty. These costs can sometimes outweigh the benefits of a lower rate, making the flexibility of a line of credit more appealing if you only need smaller amounts over time.

When a Reverse Mortgage Makes More Sense

For homeowners aged 55 and older, the choice becomes more nuanced. A home equity line of credit requires you to pass a stress test and prove you have sufficient income to manage monthly interest payments. This can be a significant hurdle for retirees on a fixed income. In these cases, a reverse mortgage Canada programme often makes more sense. Unlike a HELOC, a reverse mortgage requires no monthly payments. The loan is repaid only when you sell the home or move out. While a HELOC remains a powerful tool for those with active income, a reverse mortgage focuses on your age and equity rather than your credit score or salary, protecting your monthly cash flow during retirement.

Qualifying for a HELOC: The Broker Advantage

Qualifying for a home equity line of credit in 2026 is a rigorous process defined by the federal stress test. As previously mentioned, while the prime rate sits at 4.45 percent, lenders require you to prove you can afford payments at a much higher threshold. This isn't just about your current income; it's a measure of your financial resilience against future rate volatility. A specialized broker ensures your application is positioned to meet these criteria without unnecessary delays or rejected files.

While a credit score of 680 is the benchmark for major institutions, it isn't the only path to approval. Rachel Rogerson Mortgage Broker maintains relationships with a diverse network of B-lenders and private sources. These alternatives are crucial if your income is non-traditional or if your credit history has minor blemishes. You'll need to provide standard documentation like recent pay stubs, your most recent property tax assessment, and evidence of home insurance to verify the security of the loan for the lender.

The Application and Approval Process

The approval journey is logical and transparent. It starts with an initial consultation to review your goals, followed by a professional appraisal to confirm your home's 2026 market value. Finally, a legal professional registers the charge against your title. This structured approach prevents surprises and keeps the process moving quickly toward funding. By managing each step proactively, we ensure your time is respected and your peace of mind is maintained throughout the transaction.

Why Use a Broker Instead of Your Current Bank?

Why settle for one bank's limited menu when you can access the entire market? Unlike a single institution, Rachel Rogerson Mortgage Broker shops dozens of lenders to secure the most competitive terms. We also advocate for "unbundling," which involves placing your home equity line of credit with a different lender than your primary mortgage to maximize flexibility and avoid restrictive cross-collateralization. This concierge-level service ensures you aren't just another file in a corporate system. Ready to see how much equity you can unlock? Contact Rachel Rogerson Mortgage Broker today for a personalized strategy that puts your interests first.

Smart Strategies for Using Your Equity in 2026

Deploying your home equity line of credit requires a strategic mindset to ensure the debt works for your wealth, not against it. In the current Canadian market, one of the most effective uses is high-ROI renovations. Focus on improvements that increase the functional square footage of your home, such as finishing a basement or adding a secondary suite. These updates often pay for themselves by significantly increasing your property's resale value or providing rental income to offset borrowing costs. It's a proactive way to build equity while improving your daily living environment.

Debt consolidation remains a primary driver for many homeowners looking to streamline their finances. By shifting high-interest credit card balances or personal loans into your lower-rate credit line, you can realize immediate monthly savings. This isn't just about lower payments; it's about using those interest savings to pay down the principal balance faster. Additionally, keeping a zero-balance credit line acts as a cost-free insurance policy. It provides instant liquidity for unexpected home repairs or emergency costs without the need for high-interest loans.

For those looking to optimize their tax position, the Smith Manoeuvre is a powerful tool. It involves using your credit line for eligible income-producing investments, which can make the interest on that portion of the debt tax-deductible in Canada. This strategy effectively turns your mortgage into a tax-efficient wealth builder, though it requires precise record-keeping and professional oversight to satisfy the Canada Revenue Agency. It's a sophisticated method to build an investment portfolio using the equity you've already earned.

Investing with Home Equity

Using equity to fund a down payment on an investment property is a proven way to grow a real estate portfolio. However, you must be cautious when using a home equity line of credit during periods of market volatility. Before leveraging your equity, confirm that the projected rental income covers both the new property's expenses and the interest on your credit line. Ensure you have a buffer for potential rate changes, as variable costs can impact your net return. Intelligent investing is about calculated risks and ensuring the return exceeds your cost of borrowing.

Avoiding the HELOC Debt Trap

The flexibility of interest-only payments is a double-edged sword. It's easy to fall into the trap of never reducing the principal balance, which can lead to long-term debt cycles. To maintain financial health, establish a clear repayment plan that treats the debt like a traditional loan with a fixed end date. Rachel Rogerson Mortgage Broker can help you design a structure that prioritizes debt reduction while keeping your monthly costs manageable. Ready to see how much equity you can unlock? Pre-qualify online with Rachel Rogerson Mortgage Broker today and take control of your financial future.

Unlock Your Financial Potential with Expert Equity Strategies

Mastering your home's value is about more than just accessing cash; it's about making a strategic decision that supports your long-term wealth. You now understand how to navigate the 65 percent revolving limit and whether a home equity line of credit or a reverse mortgage best suits your current stage of life. While traditional banking often feels cold and detached, our approach focuses on your specific goals and peace of mind. We strip away the complexity to provide a clear, decisive path toward smarter financial health.

Rachel Rogerson is licensed across BC, Alberta, and Ontario, offering you direct access to more than 50 institutional and private lenders. We specialize in both traditional equity products and reverse mortgages, ensuring you receive a modernized, efficient experience tailored to your unique needs. We value your time and prioritize your financial security above all else.

Apply for your Canadian home equity line of credit in minutes to see how we can help you achieve better outcomes. Your home is your most significant investment; let's ensure it's working as hard as possible for you. We look forward to being your partner on this journey.

Frequently Asked Questions

What is the maximum I can borrow on a HELOC in Canada?

You can borrow up to 80 percent of your home's appraised value in total debt, though the revolving home equity line of credit portion is capped at 65 percent. If you have an existing mortgage, your combined loan-to-value ratio cannot exceed that 80 percent limit. This ensures you maintain a 20 percent equity stake in your property, providing a buffer against market fluctuations and protecting your long-term wealth.

Do I need to pay off my existing mortgage to get a HELOC?

You don't need to pay off your mortgage to qualify. Many Canadians use a re-advanceable mortgage that combines a standard term loan with a revolving credit line. As you pay down your mortgage principal, your available credit limit increases automatically. Alternatively, you can obtain a standalone line of credit even if your primary mortgage is held by a different lender, giving you more flexibility with your borrowing.

How do HELOC interest rates compare to standard mortgage rates?

HELOC interest rates are typically higher than standard mortgage rates because they offer greater flexibility. While a mortgage might offer a lower rate in exchange for a fixed term and strict repayment schedule, a line of credit uses a variable rate based on the prime rate plus a small margin. As of mid-2026, average rates sit around 7.63 percent, reflecting the premium paid for immediate, revolving access to funds.

Can I lose my home if I cannot pay back my home equity line of credit?

Yes, your home serves as collateral for the loan. If you consistently fail to make the required interest payments, the lender has the legal right to take possession of the property to recover their funds. It's vital to treat this credit line with the same discipline as your primary mortgage. Always ensure your budget can handle potential rate increases to protect your home ownership and your family's financial future.

Are there any hidden fees when setting up a HELOC?

While there aren't usually hidden fees, you should prepare for several upfront costs. These include a professional appraisal to determine your home's value and legal fees to register the charge on your title. Some lenders also charge a modest monthly administration fee or a title search fee. Reviewing the disclosure statement carefully helps you understand the total setup costs before you finalize the application and move forward with the process.

Can I use a HELOC to buy a second property or a cottage?

You can certainly use these funds to purchase a second property or a vacation cottage. Many investors use their primary residence's equity to cover the down payment on an investment property. This strategy allows you to expand your real estate portfolio without needing to save a large cash sum upfront. Just ensure the rental income or your personal cash flow can support the additional debt and higher interest costs.

What happens to my HELOC when I decide to sell my home?

Your home equity line of credit must be paid in full when you sell your home. Because the loan is registered against your property title, the closing lawyer will use the sale proceeds to discharge the balance before you receive the remaining equity. If you plan to move, you'll need to apply for a new credit line on your next property since these accounts aren't typically portable between different homes.

Is the interest on a Canadian HELOC tax-deductible?

Interest is only tax-deductible in Canada if you use the funds for investment purposes with the expectation of earning income. This includes buying stocks or purchasing a rental property. If you use the money for personal expenses like home renovations or debt consolidation, the interest isn't deductible. Keep meticulous records and a clear paper trail to satisfy any future audits by the Canada Revenue Agency regarding your specific deductions.