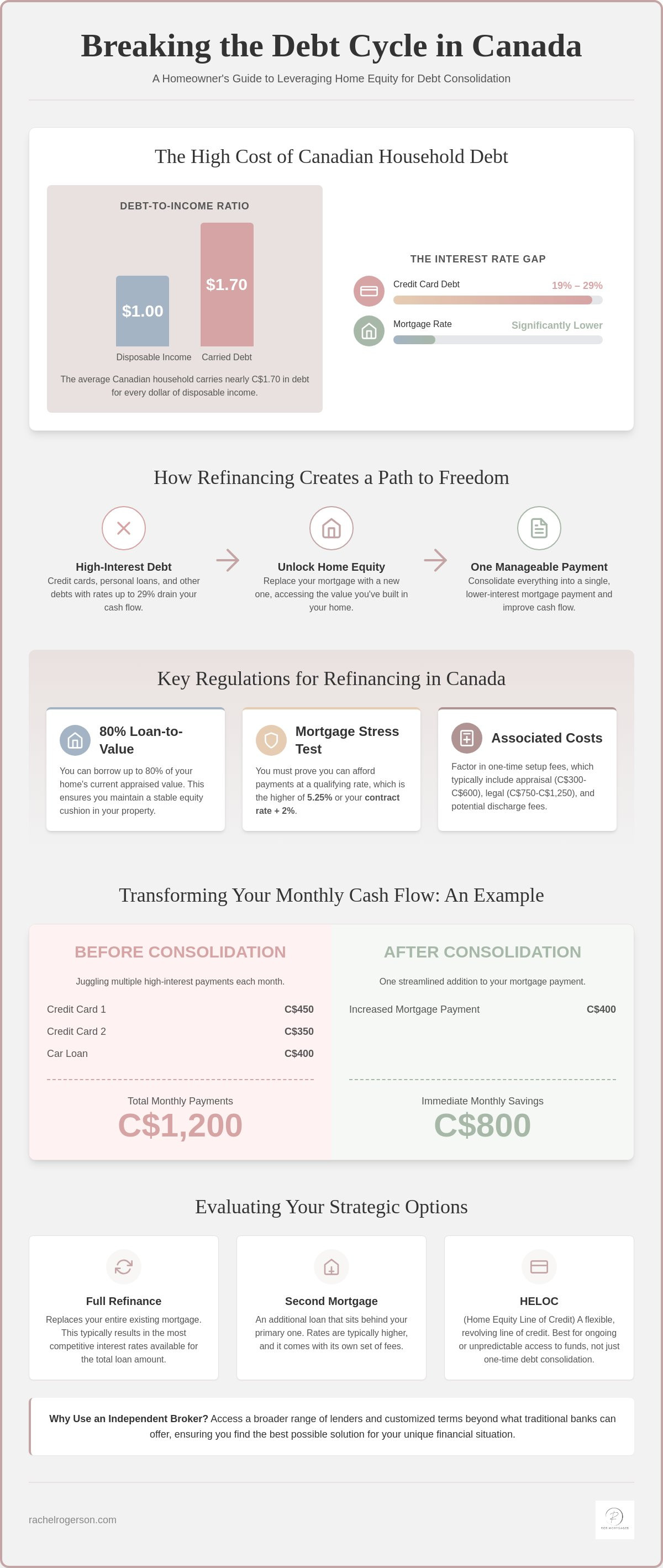

Did you know that the average Canadian household now carries nearly C$1.70 in debt for every dollar of disposable income? It’s an exhausting reality for many homeowners who feel trapped by 20 percent interest rates on credit cards while watching their monthly cash flow disappear. You might feel like you’re just running in place, but your home could be the key to breaking that cycle. When you choose to refinance to consolidate debt Canada provides a unique opportunity in 2026 to trade high-interest stress for a streamlined financial plan.

We understand that the thought of mortgage prepayment penalties or the Canadian stress test can feel intimidating. You want a clear path to becoming debt-free without the confusion of traditional banking jargon. This guide promises to show you exactly how to leverage your home equity to eliminate high-interest balances and restructure your monthly payments into one manageable sum. We will break down the current 2.25 percent Bank of Canada policy rate impact, analyze the 5.25 percent stress test requirements, and help you determine if the interest savings outweigh the costs of restructuring your mortgage today.

Key Takeaways

- Learn how to swap high-interest credit card debt for a single, lower mortgage payment to reclaim control of your monthly budget.

- Master the 80% Loan-to-Value rule and see how to refinance to consolidate debt Canada homeowners rely on to unlock built-up equity.

- Identify whether a full mortgage restructure or a flexible Home Equity Line of Credit (HELOC) better aligns with your long-term financial goals.

- Streamline your application process by learning which specific financial documents and appraisal steps are required to secure a fast approval.

- Explore the advantages of using an independent broker to access a broader range of lenders and customized terms beyond the traditional big banks.

Understanding Mortgage Refinancing for Debt Consolidation in Canada

At its core, mortgage refinancing involves replacing your existing loan with a brand new one that has entirely different terms. This process allows you to access the wealth built up in your home, often referred to as equity, and use those funds to pay off other creditors. If you are asking What is Refinancing?, it is essentially a financial reset button. Instead of juggling multiple high-interest bills, you roll them into your home loan at a much lower interest rate to simplify your life.

2026 is a pivotal year for Canadian homeowners to take action. Many people who secured historically low rates in 2021 are now facing renewals in a higher interest environment. If you find yourself in this position while also carrying consumer debt, the decision to refinance to consolidate debt Canada wide can be a strategic move to stabilize your finances. By leveraging your home equity now, you can lock in a structured plan before market conditions shift further.

The core benefit of this strategy is the massive interest gap. Most credit cards in Canada charge between 19 percent and 29 percent interest. In contrast, current mortgage rates are significantly lower. This isn't just about moving debt from one pile to another; it's about eliminating it through a smarter structure. You stop losing money to interest every month and start paying down the actual balance. This proactive approach turns a cycle of interest payments into a clear path toward financial freedom.

How Refinancing Differs from a Second Mortgage

Refinancing replaces your first mortgage entirely, which usually results in the most competitive interest rates available. A second mortgage, however, sits behind your primary loan as an additional lien. While a second mortgage might be useful if your first mortgage has a very low rate you don't want to lose, the interest rates are typically higher. You must also consider that second mortgages often come with steeper setup fees and legal costs compared to a standard refinance.

The Impact on Your Monthly Cash Flow

Consolidating high-interest payments into a single mortgage can reduce your monthly obligations by hundreds of dollars. Consider a typical Canadian household paying C$1,200 across three credit cards and a car loan; after you refinance to consolidate debt Canada, that same debt might only add C$400 to the mortgage payment. This shift creates immediate breathing room in your budget for savings or daily expenses. The psychological relief of seeing one single, manageable number on your bank statement each month provides a sense of control and optimism.

The Financial Mechanics: How Consolidating Debt Into Your Mortgage Works

Understanding the technical side of a refinance is the first step toward financial clarity. In Canada, the amount of equity you can access is strictly regulated. You can generally borrow up to 80 percent of your home's current appraised value. This limit ensures you maintain an equity cushion in your property while providing the capital needed to wipe out high-interest balances. To see how these numbers look in practice, using a Canadian Mortgage Calculator can help you visualize your potential new payment structure.

The Canadian mortgage stress test also plays a vital role in this process. Even if you aren't switching lenders, you must prove you can handle payments at the qualifying rate, which is currently the higher of 5.25 percent or your contract rate plus 2 percent. While this might seem like a hurdle, it's a protective measure for your long-term stability. When you choose to refinance to consolidate debt Canada lenders look at your entire financial profile to ensure the new loan improves your overall health rather than just shifting the burden.

Don't forget to account for the setup costs. A standard refinance involves an appraisal fee, typically C$300 to C$600, and legal fees that usually range from C$750 to C$1,250. You might also face a discharge fee from your current lender. While these upfront costs exist, they are often small compared to the thousands of dollars in interest you could save by consolidating 19 percent credit card debt into a mortgage rate closer to 4 percent. If you want to see if your equity is enough to cover these costs, you can use our mortgage calculators to run the numbers yourself.

The 80% LTV Rule Explained

To estimate your accessible equity, start with a conservative estimate of your home's value based on recent local sales. Use this formula: (Home Value x 0.80) minus your Current Mortgage Balance equals your Accessible Equity. For example, on a C$600,000 home with a C$300,000 mortgage, you could potentially access C$180,000. It's often wise to leave a small safety buffer of equity rather than borrowing the absolute maximum to protect against market fluctuations.

Calculating the Break-Even Point

The break-even point is the specific moment when the monthly interest savings from your consolidated debt exceed the one-time cost of your mortgage prepayment penalty. If your penalty is C$3,000 but you save C$500 a month in credit card interest, your break-even point is just six months. If you are within a few months of your renewal date, it might be better to wait and avoid the penalty entirely; however, if you are years away, the immediate interest savings usually justify acting now to refinance to consolidate debt Canada and stop the high-interest drain.

Evaluating Your Options: Refinance vs. HELOC vs. Second Mortgages

Choosing the right financial tool depends on your specific mortgage rate and long-term goals. If you choose to refinance to consolidate debt Canada homeowners often find that a full mortgage replacement is the most straightforward path. It provides a single, fixed interest rate and a clear end date for your debt. This is especially effective if you are dealing with a large volume of high-interest debt that requires a disciplined repayment schedule and a predictable monthly obligation.

A "blend and extend" is another option offered by many Canadian lenders. This allows you to access equity without breaking your current term and paying a massive penalty. The lender averages your existing low rate with current market rates to create a new, mid-range rate. It’s a practical middle ground if you are mid-term and want to avoid the "break-even" calculations we discussed earlier while still accessing the funds needed to clear your high-interest balances.

A second mortgage is a tactical choice specifically for those who hold a "unicorn" low interest rate on their primary mortgage. If your first mortgage is locked in at a rate well below current market averages, it rarely makes sense to refinance the entire balance into a higher 2026 rate. Instead, a second mortgage sits behind your primary loan. While the interest rate on this second piece will be higher, the weighted average of both loans might still be lower than a full refinance. This allows you to keep your primary low rate intact while still tapping into equity.

When to Choose a HELOC for Debt Consolidation

A Home Equity Line of Credit (HELOC) offers unmatched flexibility because you only pay interest on the funds you actually use. Modern "readvanceable" mortgages even allow your HELOC limit to increase automatically as you pay down your mortgage principal. However, keep in mind that Canadian regulations limit the revolving portion of a HELOC to 65 percent of your home's value. You need a high level of financial discipline here; if you treat the HELOC like a credit card, you risk "re-loading" the debt you just tried to eliminate.

Private Mortgages: A Bridge to Better Credit

Sometimes, traditional banks might hesitate if your credit score has already taken a hit from high-interest balances. In these cases, private mortgages serve as an essential "bridge" to better financial health. These are short-term solutions, typically one to two years, designed to consolidate your debt immediately and give your credit score time to recover. Taking a private mortgage requires a solid exit strategy. This usually involves improving your credit profile enough to move back to a traditional lender at the end of the term. Rachel Rogerson Mortgage Broker specializes in navigating the private lending landscape across Canada, ensuring you have a clear, professional plan to return to "A" lending as quickly as possible. This temporary move can be the catalyst you need to finally refinance to consolidate debt Canada and reclaim your financial momentum.

Step-by-Step: How to Refinance Your Canadian Mortgage to Consolidate Debt

Executing a successful refinance requires more than just a good credit score; it demands a methodical approach to your paperwork and a clear understanding of current lending standards. As we move through 2026, Canadian lenders have become more meticulous in their review process. To refinance to consolidate debt Canada homeowners must prove they can navigate the 5.25 percent stress test while maintaining enough equity to cover their existing mortgage and all outstanding high-interest balances. This section provides a clear roadmap to take you from a state of financial stress to a streamlined, single-payment reality.

The process begins with an honest assessment of your current liabilities. You need to gather every credit card statement, car loan agreement, and line of credit balance you intend to clear. This isn't just for your own organization; lenders need to see exactly where the funds are going to ensure the consolidation truly improves your debt-to-income ratio. Once your application is submitted through a professional broker, you will receive a mortgage commitment. This document outlines your new interest rate and terms. After you sign, your legal representative handles the discharge of your old debts, ensuring those high-interest accounts are paid in full directly from the refinance proceeds. If you're ready to see how these steps apply to your specific situation, you can start your refinance application today and get expert guidance on every document required.

Preparing Your Documentation for 2026 Standards

Lenders are looking closer at proof of income than they did a few years ago. You will need your two most recent T4 slips and, more importantly, your latest Notice of Assessment (NOA) from the CRA to confirm no taxes are owing. If you're self-employed, expect to provide two years of full tax returns and potentially your business financial statements. Organizing these early prevents delays that could cause you to miss out on a favourable rate lock during a volatile market week.

Navigating the Appraisal Process

A professional appraisal is the linchpin of your refinance because it confirms your 80 percent Loan-to-Value limit. To ensure your home appraises at its maximum fair market value, treat the appraiser's visit like an open house. Clear away clutter, finish minor repairs, and provide a list of recent upgrades like a new roof or HVAC system. If an appraisal comes in lower than expected, don't panic. A skilled broker can often challenge the results with better comparable sales or look for a different lender whose appraisal panel understands your specific neighbourhood better. This step is critical to ensure you have enough accessible equity to refinance to consolidate debt Canada wide without having to leave any high-interest balances behind.

Strategic Debt Management: Why an Independent Broker Outperforms the Banks

While your bank advisor is a representative of a single institution, an independent broker is an advocate for your specific financial outcome. When you choose to refinance to consolidate debt Canada homeowners often find that banks are bound by rigid internal policies that don't account for the unique market shifts of 2026. A broker, however, operates with a concierge mindset, prioritizing your long-term health over a single bank's quarterly targets and internal risk quotas.

Access to over 30 lending institutions, including credit unions and monoline lenders, creates a competitive environment that works in your favour. This variety ensures you aren't just getting a rate, but the most strategic structure for your specific equity position. The process is modern and streamlined, utilizing tech-savvy tools to respect your time while maintaining the human touch that traditional banking often lacks. We move quickly from identifying your needs to providing a clear, decisive path forward.

Customized Solutions for Complex Situations

Standard bank algorithms often fail to capture the complexity of self-employed earners or those navigating a temporary credit dip. Whether you are in the high-demand regions of BC and Ontario or the evolving markets of Alberta, localized expertise is essential. A "no" from a big bank is frequently just the beginning of a conversation with Rachel Rogerson Mortgage Broker, where we look for the "yes" among a much wider pool of lenders who specialize in non-traditional applications.

Achieving Peace of Mind with Rachel Rogerson Mortgage Broker

Refinancing your home is a significant decision that requires both specialized knowledge and a supportive guide. We provide a professional experience that strips away the intimidation of complex financial transactions, replacing it with clarity and momentum. Pre-qualify online today to see how much equity you can unlock with our efficient, 60-second process and start your journey toward smarter financial health and lasting peace of mind.

Secure Your Financial Future and Reclaim Your Cash Flow

Your home is a significant asset that should serve your life goals rather than just being a monthly expense. By choosing to refinance to consolidate debt Canada homeowners can turn stagnant equity into active financial relief. This isn't just about managing numbers; it's about reclaiming the mental space that high-interest debt consumes every single day. You've seen the mechanics and the potential savings, and now the opportunity to restructure your future is within reach.

Navigating this transition requires a partner who understands the intricacies of the Canadian lending landscape. Rachel Rogerson Mortgage Broker is licensed across BC, Alberta, and Ontario, providing access to institutional and private lenders that traditional banks simply cannot reach. Whether you are dealing with complex refinancing needs or looking into reverse mortgages, we offer the specialized expertise required to protect your equity while meeting your cash flow objectives. We remain committed to being your guide through every step of this modern, efficient process.

Take control of your financial narrative today and stop the drain of high-interest payments. Take the first step toward debt freedom; pre-qualify online in 60 seconds. You have worked hard to build the equity in your property; now let us help you use it to create the financial freedom you deserve. Your path to a streamlined, stress-free budget starts with a single click.

Frequently Asked Questions

What is the maximum amount I can borrow when I refinance to consolidate debt in Canada?

You can typically borrow up to 80 percent of your home's appraised value in Canada. This limit is set by federal regulations to ensure a 20 percent equity buffer remains in the property. To calculate your specific limit, multiply your current home value by 0.80 and subtract your existing mortgage balance. This remaining amount represents the equity available to refinance to consolidate debt Canada wide.

Will refinancing to consolidate debt hurt my credit score?

Refinancing causes a temporary, minor dip in your credit score due to the hard inquiry performed by the lender. However, the long-term impact is overwhelmingly positive. By paying off high-interest credit cards, you significantly lower your credit utilization ratio. This shift often leads to a substantial score increase within a few months of consolidating your debt into a single, lower-interest mortgage payment.

How much does it cost to break my mortgage for debt consolidation?

The cost depends on whether you have a fixed or variable-rate mortgage. For variable-rate loans, the penalty is usually three months of interest. For fixed-rate loans, lenders charge the greater of three months of interest or the Interest Rate Differential (IRD). You should also factor in appraisal fees of C$300 to C$600 and legal fees between C$750 and C$1,250 to complete the transaction.

Can I refinance my mortgage if I am self-employed or have bad credit?

Yes, you can still qualify by working with an independent broker who has access to alternative and private lenders. While traditional banks have rigid criteria, many other institutions specialize in stated-income programs for the self-employed or equity-based lending for those with bruised credit. These solutions often serve as a bridge to help you repair your credit before eventually moving back to a prime lender.

Is it better to use a HELOC or a full refinance for debt consolidation?

A full refinance is usually better for consolidating a large, one-time sum of debt into a predictable, fixed monthly payment. A Home Equity Line of Credit (HELOC) is a revolving product that offers more flexibility and interest-only payment options. If you need a disciplined structure to ensure the debt is actually paid off, a full refinance to consolidate debt Canada is typically the safer strategic choice.

How long does the mortgage refinancing process take in Canada?

The refinancing process generally takes between two to four weeks from your initial application to the funding date. This timeline includes the time needed for a professional appraisal, lender underwriting, and the legal work performed by your lawyer. Being organized with your T4s, NOAs, and debt statements can help speed up the approval process and ensure a smooth closing.

Do I have to pay the stress test when I refinance my mortgage?

You must pass the Canadian mortgage stress test when you refinance to access equity or switch lenders. You will need to qualify at the higher of 5.25 percent or your actual contract rate plus 2 percent. This requirement ensures you can still manage your payments if interest rates rise in the future. It is a mandatory step for all regulated lenders in Canada when restructuring a mortgage.

What happens to my amortization period when I consolidate debt into my mortgage?

Your amortization period typically resets when you refinance; it can be extended up to 25 or 30 years depending on your equity. Stretching the amortization lowers your monthly payment and improves your immediate cash flow. However, it is important to remember that a longer period means you will pay more in total interest over the life of the loan unless you make extra principal payments.