What if the lowest advertised number isn't actually the cheapest way to tap into your home's value? Many Canadian seniors feel the weight of the rising cost of living in 2026, making the search for the best reverse mortgage interest rates Canada has to offer more critical than ever. It's natural to worry about how compounding interest might affect your estate or if you'll eventually lose the house to a lender. You've worked hard to build your equity; you deserve a solution that protects it while providing the cash flow you need.

We understand that the math behind these products can feel intimidating and opaque. This guide simplifies the process by showing you exactly how to analyze the current 2026 rate landscape and compare top lenders like HomeEquity Bank and Equitable Bank. You will discover how to minimize long-term borrowing costs and keep more equity for your heirs. We'll break down current fixed and variable options, explain the impact of compounding interest, and highlight the specific strategies that help you secure the most intelligent financial path forward for your retirement.

Key Takeaways

- Learn how to evaluate reverse mortgage interest rates Canada in the current 2026 market to ensure you aren't paying more than necessary for your equity release.

- Understand the mechanics of semi-annual compounding interest and how it differs from traditional debt to protect your long-term home equity.

- Compare the benefits of locking in a fixed rate versus choosing a variable option that fluctuates with the Canadian Prime Rate.

- Discover how factors like your age and property location can significantly increase your borrowing limit and improve your available terms.

- See why partnering with a specialized mortgage broker provides access to unposted rate specials that traditional banks often keep hidden.

Current Landscape of Reverse Mortgage Interest Rates in Canada

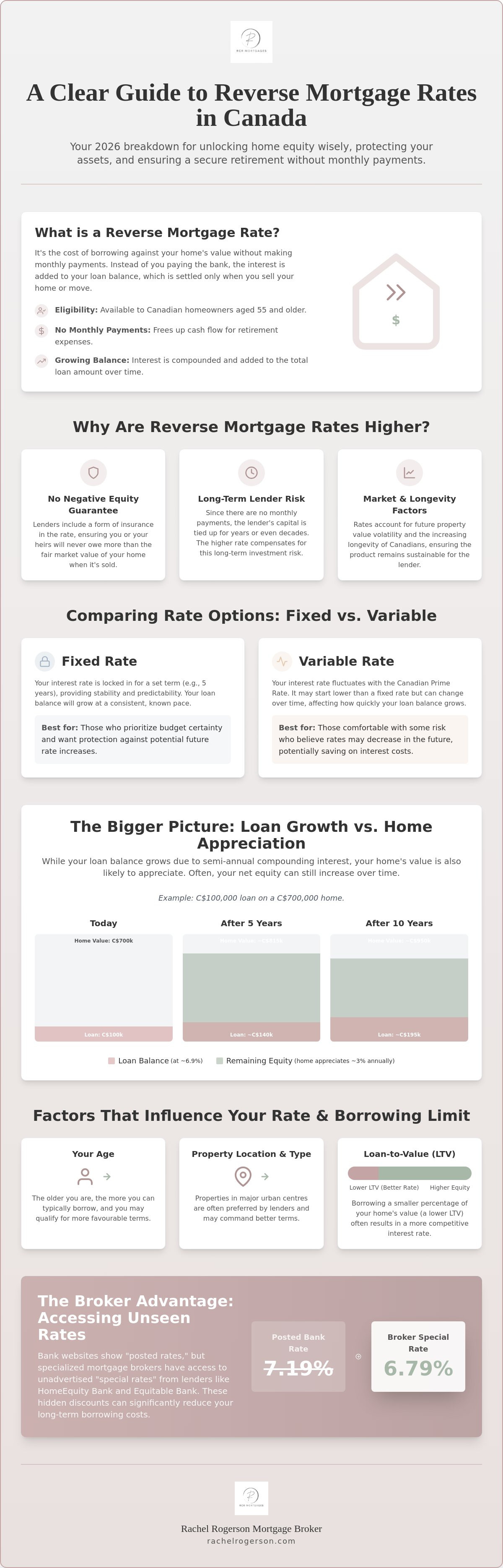

Think of What is a Reverse Mortgage interest rate as the cost of unlocking the wealth you've built in your home without the burden of monthly payments. For Canadian homeowners aged 55 and older, this is known as equity release. Unlike a traditional mortgage where you pay down the principal, reverse mortgage interest rates Canada represent a debt that grows over time. As of July 2026, the market is primarily served by established lenders like HomeEquity Bank and Equitable Bank, alongside specialized providers such as Home Trust. The current rate environment reflects a specialized financial product that prioritizes your immediate cash flow over long term debt reduction.

Interest in this market is not paid out of pocket each month. Instead, it is added to your loan balance in a process known as compounding. This means you keep your cash for daily living expenses while the lender waits for the loan to be settled when you eventually sell the home, move, or pass away. While these rates are higher than standard 5-year fixed mortgages, the "premium" you pay buys you the right to stay in your home without a monthly bill. It's a strategic trade-off that has become increasingly popular as the cost of living in 2026 continues to challenge retirement budgets.

Why Reverse Mortgage Rates are Higher Than Traditional Mortgages

Lenders charge more for these products because they are taking on significantly more risk. When you don't make monthly payments, the lender's capital is tied up for years, sometimes decades. They also provide a "No Negative Equity" guarantee. This ensures that you or your heirs will never owe more than the fair market value of the home, regardless of how much interest accumulates. This insurance is built directly into the rate. In the 2026 market, lenders must also account for property value volatility and the increasing longevity of Canadian seniors. You are paying for the security of knowing your housing is permanent.

2026 Rate Trends: What Homeowners Need to Know

The Bank of Canada's overnight rate remains a key driver for all borrowing costs, but reverse mortgage terms have their own unique rhythm. You'll often see a noticeable gap between "posted rates" found on bank websites and the "special" rates available through professional broker channels. These discounts are often substantial. Waiting for a theoretical "perfect" rate can be a costly mistake. If inflation or property taxes rise faster than the interest rate drops, the delay could cost you more in lost buying power than you save on interest. Taking a proactive approach allows you to secure your financial health today.

How Reverse Mortgage Interest is Calculated and Compounded

Understanding the math behind your loan is the best way to maintain control over your financial future. In Canada, the standard for calculating mortgage interest is semi-annual compounding. This means the lender calculates the interest twice per year rather than every month. Compounding interest is the process where interest is charged on the previous period's accumulated interest plus the principal. While most traditional investments focus on simple interest, reverse mortgages use this compounding structure to allow you to defer payments indefinitely.

Your specific rate is often influenced by your Loan-to-Value (LTV) ratio. This ratio represents how much you are borrowing compared to the total appraised value of your home. Lenders typically offer more competitive reverse mortgage interest rates Canada to borrowers with lower LTV ratios. If you only need to access 20% of your home's value, you may find more favourable terms than someone looking to maximize their borrowing at 55%. This risk based pricing ensures that the product remains sustainable for both you and the lender. You can use a mortgage calculator to see how different LTV scenarios impact your long term equity.

The Math of Compounding: A 10-Year Outlook

Visualizing the growth of your balance helps remove the mystery from the process. If you take a C$100,000 advance at a 2026 average rate of 6.5%, your balance won't stay at that level for long. After ten years, that C$100,000 grows significantly as the interest begins to "interest on interest." However, it is vital to consider property appreciation. If your home's value increases by 3% or 4% annually, your total net equity might actually grow even while the loan balance increases. The frequency of compounding matters too; semi-annual compounding results in a slightly lower total cost compared to the monthly compounding often found in other types of debt.

Interest vs. APR: Understanding the Total Cost of Borrowing

The "headline rate" you see in advertisements is rarely the whole story. To understand the true cost, you must look at the Annual Percentage Rate (APR). The APR is the "all-in" cost of borrowing. It includes the base interest rate plus mandatory setup costs like appraisal fees, which range from C$300 to C$600, and independent legal advice. According to the Financial Consumer Agency of Canada guidelines, lenders must be transparent about these costs. High setup fees can make a low interest rate more expensive over a short period. Always compare the APR when shopping between lenders to ensure you're getting the most efficient deal for your specific timeline.

Comparing Fixed vs. Variable Reverse Mortgage Rates

Choosing between a fixed or variable term is perhaps the most significant decision you'll make when setting up your equity release. While traditional banks offer standard mortgages, the reverse mortgage market in Canada is more specialized. Most retirees find themselves comparing options from various lenders, such as the long-term stability offered by HomeEquity Bank or the competitive flexibility from Equitable Bank. Each provider structures their fixed and variable products differently; the right choice depends entirely on your 2026 financial outlook and personal circumstances. Understanding reverse mortgage interest rates Canada requires looking past the headline number to see how the term length matches your lifestyle goals. Consulting with an experienced professional, such as Rachel Rogerson Mortgage Broker, can help clarify these choices.

It's also essential to distinguish between "Open" and "Closed" terms. A closed term usually offers a lower rate but carries higher penalties if you decide to pay off the mortgage early or move. An open term provides maximum flexibility, allowing you to refinance or sell the property with minimal friction. As highlighted in the Financial Consumer Agency of Canada guide, these structural details often matter more than a fraction of a percentage point in the interest rate itself.

When to Choose a Fixed Interest Rate

- Budget certainty: Fixed rates are ideal if you're on a strict pension income and want to know exactly how your debt will grow. You can lock in your rate for 1, 3, or 5 years.

- Inflation protection: If you believe the economic climate in 2026 and 2027 will remain volatile, locking in a rate now prevents your borrowing costs from spiking later.

- The trade-off: Fixed terms typically start at a higher initial rate than variable options. You're paying a small premium for the peace of mind that your rate won't change.

The Case for Variable Reverse Mortgage Rates

- Lower starting points: Variable rates often begin lower than fixed rates. If market interest rates decline during your retirement, your loan balance will grow more slowly.

- Greater flexibility: Variable terms, such as the 5-year adjustable options from Home Trust or Equitable Bank, often come with more lenient prepayment privileges. This is helpful if you plan to downsize in the near future.

- Risk tolerance: This path is best for homeowners who can handle the uncertainty of rate hikes. If the Canadian Prime Rate rises, the interest added to your loan balance will increase immediately.

Before committing, evaluate your 10-year plan. If you intend to stay in your home for the rest of your life, a 5-year fixed rate provides a solid foundation. However, if you're using a reverse mortgage as a "bridge" before a future move, a variable or shorter-term fixed rate might offer the agility you need without heavy exit fees.

Factors That Influence Your Specific Rate and Borrowing Limit

Securing the best reverse mortgage interest rates Canada offers isn't just about timing the market; it's about how you present your profile to the lender. Unlike a traditional mortgage where your salary is the star of the show, a reverse mortgage cares more about the asset and the person holding the title. This "no-income" advantage means your credit score and monthly earnings take a back seat. Lenders focus instead on the stability of your home's value and your life expectancy. This shift in focus is why many retirees find these products more accessible than a standard Home Equity Line of Credit (HELOC) during their non-earning years.

Each lender has a specific "appetite" for different scenarios. For instance, some banks might prefer high-density urban condos, while others offer more aggressive terms for detached homes in established neighbourhoods. In 2026, we see lenders becoming more surgical with their risk assessments. They look at regional market trends to decide how much equity they're willing to release. If your property is in a highly sought-after urban centre, you'll likely see higher borrowing limits compared to a rural property where resale might take longer.

How Age Impacts the Interest Rate Spread

The "Age Rule" is the most influential factor in your quote. Lenders use actuarial math to determine risk. Simply put, the older the borrower, the shorter the expected duration of the loan. This reduced timeline means there is less time for interest to compound and potentially exceed the home's value. An 80-year-old borrower will almost always qualify for a higher Loan-to-Value (LTV) ratio than a 55-year-old. For couples, lenders usually base the qualification on the age of the youngest spouse. If there is a significant age gap, it pays to strategize. Sometimes waiting a year or two for the younger spouse to reach a specific age bracket can unlock significantly better terms.

Property Valuations in the 2026 Canadian Market

Your journey to a better rate starts with an accurate appraisal. In the 2026 market, lenders are looking for properties that are well-maintained and easy to sell. Minor details like "curb appeal" or a recent roof replacement can actually influence the lender's risk assessment. A home in disrepair represents a higher risk of losing value over time, which might lead to a less favourable rate or a lower borrowing cap. Before you book an appraisal, ensure your home is presented in its best light. If you want to see how much equity you can access based on your current age and home value, get a personalized quote today to compare your options across all major Canadian lenders.

Why Working with a Mortgage Broker Secures the Best Rate

Many seniors assume that their decades of loyalty to a primary bank will automatically translate into the best financial terms. This is a common mistake that can lead to significantly higher borrowing costs. While your local branch only has access to one set of proprietary products, a specialized mortgage broker scans the entire market. Finding the most competitive reverse mortgage interest rates Canada provides requires a neutral comparison of all available options. We act as your advocate, ensuring you don't settle for the first offer you receive.

Brokers provide a concierge level of service that handles the heavy lifting of the application process. From coordinating the mandatory appraisal to ensuring you have access to independent legal advice, we streamline every step. This professional oversight prevents common delays and ensures that the paperwork is handled with precision. It's about more than just a number; it's about making sure the loan fits your broader tax and estate planning goals. We look at the big picture to ensure your equity release doesn't negatively impact your OAS or GIS benefits.

The Independent Advantage vs. Big Bank Loyalty

Bank loyalty often results in paying posted rates that are designed for the general public. In contrast, an independent broker can show you products from multiple major Canadian lenders side-by-side. This transparency exposes hidden fees that direct lenders might bury in complex documentation. Because brokers leverage high transaction volumes, they often gain access to unposted rate specials that aren't advertised on bank websites. This insider access is a powerful tool for protecting your home equity and reducing the long term cost of borrowing.

Customizing Your Equity Release Strategy

Your payout structure is just as important as the interest rate itself. You might choose a single lump sum for a major home renovation or opt for planned advances that provide a steady monthly income. Each choice changes how interest accumulates over the life of the loan. We help you integrate a reverse mortgage with your existing HELOC or investment portfolio to maximize your cash flow while minimizing tax implications. This tailored approach ensures that your home remains a source of strength rather than a source of stress. Book a free consultation with Rachel Rogerson Mortgage Broker to compare 2026 reverse mortgage rates today.

Take Control of Your Retirement Equity

Securing the most competitive reverse mortgage interest rates Canada offers requires more than just a quick search. It's about understanding how semi-annual compounding affects your long term balance and choosing between the stability of a fixed rate or the potential savings of a variable term. You've worked hard to build your home equity. Now, it's time to make that equity work for you without the fear of losing your home or your independence.

As Rachel Rogerson Mortgage Broker, I provide neutral access to all major Canadian lenders across the BC, Alberta, and Ontario markets. My goal is to deliver a transparent, no-obligation assessment that aligns with your specific estate goals. You don't have to navigate these complex financial waters alone. We can find a solution that protects your heirs while providing the cash flow you need for a comfortable retirement.

Ready to see your options? Get your personalized reverse mortgage rate quote in 60 seconds and take the first step toward a smarter financial future. Your home is your greatest asset; let's treat it that way.

Frequently Asked Questions

Is the interest on a Canadian reverse mortgage tax-deductible?

In most cases, the interest is not tax-deductible because it isn't being paid out of pocket on a regular basis. However, if you use the loan proceeds specifically to invest in income-producing assets, you may be able to deduct the interest costs. We recommend consulting with a qualified tax professional to see how this applies to your specific 2026 financial plan.

Can the interest rate on my reverse mortgage change after I sign?

Your rate will only fluctuate if you choose a variable or adjustable term. If you select a fixed-rate product, your rate is locked for the duration of that term, such as 1, 3, or 5 years. Once that term expires, you will renew at the prevailing reverse mortgage interest rates Canada offers at that time. This allows you to choose the level of budget certainty that fits your comfort zone.

What happens if the interest eventually exceeds the value of my home?

You are protected by a "No Negative Equity" guarantee provided by all major Canadian lenders. As long as you maintain the property, pay your taxes, and keep your insurance current, you will never owe more than the fair market value of the home. If the house sells for less than the loan balance, the lender absorbs the loss rather than passing it to you or your heirs.

Are reverse mortgage rates higher in Ontario compared to BC or Alberta?

Base interest rates are typically consistent across Ontario, BC, and Alberta. While your specific location can influence your maximum borrowing limit or Loan-to-Value (LTV) ratio, the interest rate itself is generally set at a national level by lenders like HomeEquity Bank and Equitable Bank. Regional differences are more likely to appear in property appraisal values rather than the interest percentage.

How often is interest calculated on a CHIP or EQ Bank reverse mortgage?

Interest is calculated and compounded semi-annually, which is the standard practice for mortgages in Canada. This means the interest is added to your principal balance twice per year. This compounding frequency is actually more favourable for the borrower than monthly compounding, as it results in a slightly slower growth of the total loan balance over time.

Can I pay off the interest monthly to stop the balance from growing?

Yes, most lenders provide the flexibility to make interest-only payments. While the defining feature of a reverse mortgage is that no monthly payments are required, you can choose to pay down the interest or even a portion of the principal annually. This is an excellent strategy for homeowners who want to access cash now while preserving as much equity as possible for their estate.

What are the typical closing costs associated with a reverse mortgage in 2026?

You should budget for an appraisal fee between C$300 and C$600 and independent legal advice ranging from C$300 to C$700. Lenders also charge administrative setup fees that are typically deducted from your mortgage proceeds. For example, Equitable Bank currently charges a C$995 setup fee, while Bloom has a flat processing fee of C$1,650. These costs ensure the transaction is handled transparently and legally.

Will a reverse mortgage affect my OAS or GIS government benefits?

A reverse mortgage has no impact on your Old Age Security (OAS) or Guaranteed Income Supplement (GIS) payments. The funds you receive are considered a loan advance rather than earned income, so they are completely tax-free. This allows you to supplement your lifestyle or cover healthcare costs without triggering any clawbacks or reductions in your hard-earned government entitlements.